Thomas J Catalano is an effective CFP and you will Inserted Investment Adviser with the condition of South carolina, in which the guy revealed his or her own monetary advisory organization when you look at the 2018. Thomas’ sense provides your knowledge of several section together with assets, advancing years, insurance rates, and you can economic believe.

What exactly is a beneficial Subprime Financing?

A good subprime loan is a type of loan available at good rate a lot more than primary to individuals that do maybe not qualify for prime-rate funds. Oftentimes subprime individuals have been refused from the antique lenders for their reduced credit scores and other factors one recommend he’s a good likelihood of defaulting on personal debt fees.

Key Takeaways

- Subprime financing keeps interest rates which might be greater than the prime rates.

- Subprime individuals are apt to have lower credit ratings otherwise is actually those who was perceived as attending default into that loan.

- Subprime interest levels can differ one of loan providers, making it a smart idea to shop around before you choose one.

Exactly how an excellent Subprime Financing Functions

Whenever banking companies lend one another money in the middle of brand new nights to cover the set-aside criteria, they costs both the prime price, mortgage loan in line with the government funds rates based of the the new Federal Open market Committee of one’s Federal Set-aside Financial. Just like the Fed’s site demonstrates to you it, « Although the Government Set-aside has no head part within the setting the newest finest rate, of several banking institutions desire set their finest prices oriented partially into the the prospective level of the brand new government funds price-the speed that finance companies fees one another having small-label finance-built from the Federal Open-market Committee. »

The top price has fluctuated from a reduced out of dos% in the 1940s to help you a top regarding 21.5% regarding the eighties. At their , Federal Open-market Committee (FOMC) fulfilling, the fresh Government Reserve decreased the goal range toward given financing speed in order to 0%0.25%. This task is the consequence of the new Government Reserve’s services to combat the economic consequences of one’s COVID-19 pandemic. While the 1990’s, the top rates has typically been set-to 3 hundred base points above the given money rate, translating to a Hudson pay day loans primary rate of 8.5% according to the Fed’s most recent action, during this creating.

The prime rate takes on a giant part from inside the deciding the attention you to banking companies fees their consumers. Usually, businesses or any other financial institutions found prices equivalent or really personal toward primary rate. Merchandising customers that have good credit and good borrowing records taking away mortgages, home business funds, and car loans discovered cost a bit higher than, but predicated on, the prime speed. Applicants with low fico scores and other exposure things are given prices from the loan providers which can be somewhat greater than the top rates-and this the word subprime financing.

More lenders e trend. This means a good subprime mortgage borrower has actually a chance to save your self some cash because of the shopping around. Still, by the definition, most of the subprime financing cost are more than the top rate.

Together with, borrowers you will occur to hit with the subprime credit ple, answering a marketing getting mortgages when they in reality qualify for a better price than just he could be given after they follow up towards the post. Borrowers should check to see whether they be eligible for an effective most useful rate compared to one to he is in the first place provided.

The higher rates of interest toward subprime financing can result in 10s away from several thousand dollars during the additional focus payments along the lifetime from financing.

Special Factors to own Subprime Financing

To the higher-label fund, such as mortgage loans, the other percentage tourist attractions often change so you can tens regarding thousands of dollars property value even more appeal repayments along the life of your mortgage. This can build repaying subprime money hard for reasonable-money borrowers, as it did throughout the later 2000s. In the 2007, high numbers of individuals carrying subprime mortgage loans started initially to default. Ultimately, so it subprime meltdown try a significant factor with the overall economy therefore the resulting Higher Credit crunch. This is why, a great amount of larger banking companies had out of the subprime financing team. Now, even if, this has arrive at transform.

When you are any lender can offer that loan with subprime prices, you can find loan providers that focus on 2nd-chance finance and you can subprime funds with high prices. Perhaps, these lenders promote consumers that issues delivering low interest the ability to availability money to blow, expand its enterprises, otherwise pick home.

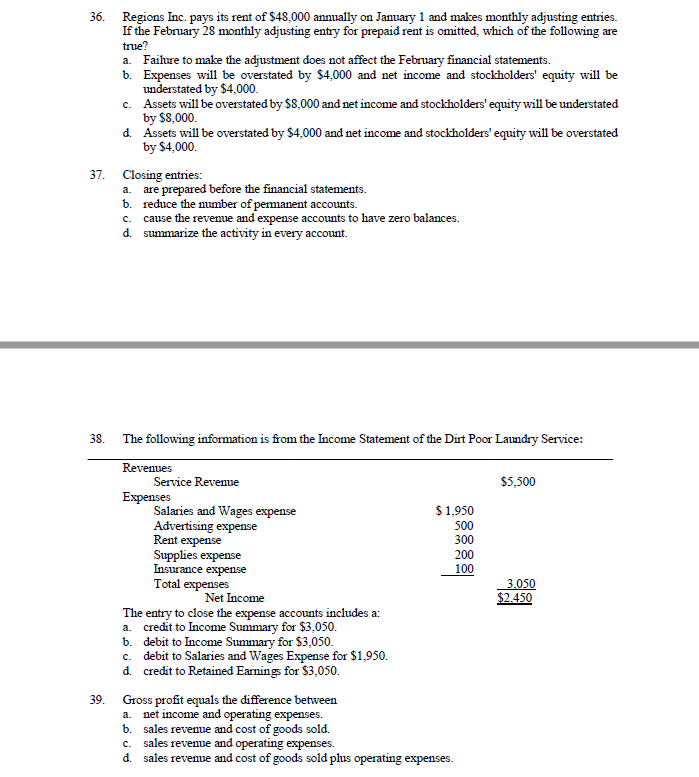

Subprime lending is usually considered predatory credit, the habit of offering borrowers money which have unrealistic costs and securing them into financial obligation otherwise growing its odds of defaulting. However, providing an effective subprime mortgage is a sensible alternative if your loan is meant to repay bills having large rates of interest, such as for example credit cards, or if this new debtor doesn’t have other technique of obtaining borrowing.